SK Hynix, the South Korean memory chipmaker powering the AI boom, is preparing to list on US exchanges at $166 per share - but HSBC analysts think American investors are getting a bargain. The bank's latest research note suggests the stock could climb 20% higher once it starts trading stateside, finally closing the persistent valuation discount against rival Micron Technology. It's a bet that US markets will wake up to what Asian investors already know: SK Hynix isn't just making memory chips anymore, it's manufacturing the AI infrastructure everyone's scrambling to buy.

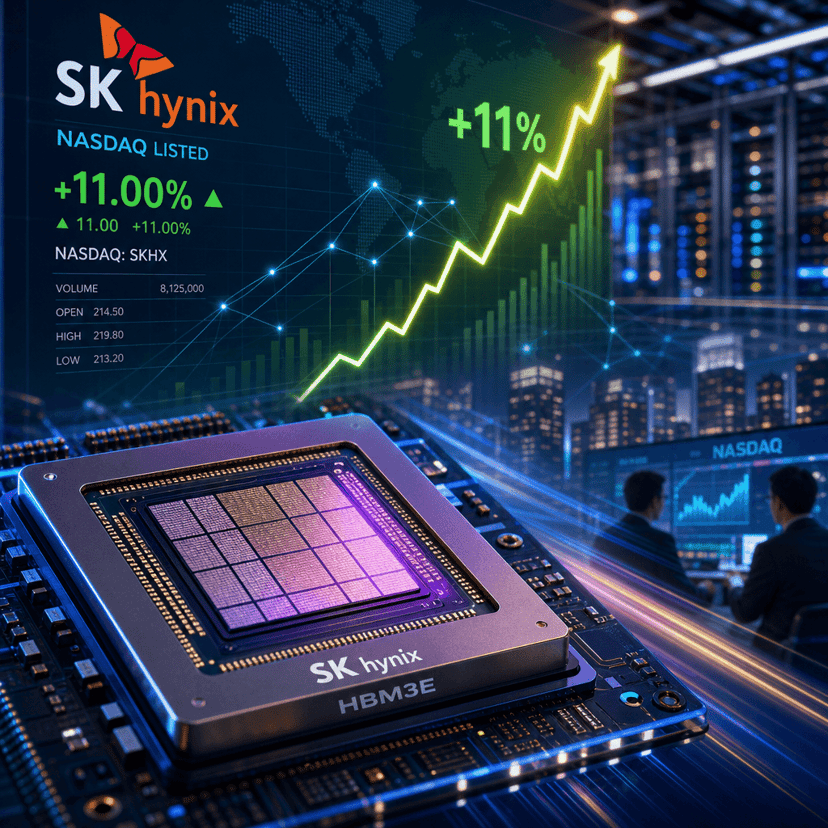

SK Hynix is about to test whether American investors will pay up for the memory chips running the AI revolution. The South Korean semiconductor giant is gearing up for a US listing priced at $166 per share, according to HSBC research cited by CNBC. But here's the kicker - the bank's analysts think that's just the starting line, projecting the stock could rally another 20% as US investors finally recognize what their Asian counterparts have known for months.

The move comes as SK Hynix dominates one of the hottest corners of the chip market: high-bandwidth memory, or HBM, the specialized chips that sit next to AI processors in data centers. While Micron Technology has enjoyed premium valuations trading on US exchanges, SK Hynix has languished at a discount despite shipping the majority of HBM chips going into Nvidia's H100 and H200 AI accelerators. HSBC sees the US listing as the catalyst to flip that script.

"The foray into US markets" will help narrow the valuation gap, HSBC analysts noted in their research. It's not hard to see why they're bullish. SK Hynix has essentially become the pick-and-shovel play for the AI infrastructure buildout, with its HBM3E memory becoming as critical to AI performance as the GPUs themselves. The company's been sold out of HBM capacity for quarters, with customers lined up and willing to pay premium prices.

The $166 entry price values SK Hynix at roughly 8-9 times forward earnings based on consensus estimates - a meaningful discount to Micron's double-digit multiple. That gap exists partly because of home market dynamics. South Korean stocks traditionally trade at lower valuations than US peers, a phenomenon known as the "Korea discount" that stems from concerns about corporate governance, geopolitical risks with North Korea, and lower liquidity in Seoul's market.

But HSBC's 20% upside call to roughly $200 per share suggests those concerns will matter less once SK Hynix gets NYSE or Nasdaq ticker symbols flashing across Bloomberg terminals. US institutional investors have been underweight Korean semiconductors not because of fundamentals, but because of accessibility and familiarity. A US listing changes that equation overnight.

The timing looks deliberate. Memory chip prices have stabilized after a brutal downturn in 2023, and the AI boom has created a new premium tier for advanced products like HBM3E. Samsung, SK Hynix's crosstown rival, is scrambling to catch up in HBM production after initially dismissing the market. That leaves SK Hynix with a comfortable lead in the one memory category where supply can't keep up with demand.

Investors should watch how the company positions its growth story for American audiences. SK Hynix has traditionally been seen as a cyclical commodity producer, riding the boom-bust waves of DRAM and NAND pricing. But the HBM business model looks different - longer-term supply agreements, stickier customer relationships, and structural demand from AI infrastructure that isn't going away after one product cycle.

The competitive landscape adds another wrinkle. Micron has been pitching itself as the American answer to Asian memory dominance, winning subsidies and support for domestic production. SK Hynix's US listing could complicate that narrative, offering American investors direct exposure to the actual market leader in AI memory without the "buy American" premium.

There's also the question of what SK Hynix does with the increased visibility and potentially higher valuation that comes with a US listing. The company could use its stock as currency for acquisitions, partnerships, or talent recruitment in Silicon Valley. Access to US capital markets also provides flexibility for future fundraising as it expands HBM production capacity.

HSBC's price target assumes US investors will apply similar valuation multiples to SK Hynix that they currently give Micron, adjusting for growth rates and market position. Given SK Hynix's lead in HBM and its position as Nvidia's primary memory supplier, that re-rating looks entirely plausible once American funds can easily add the stock to their portfolios.

The $166 starting price gives institutions a clear entry point, and the 20% upside projection provides enough potential return to justify the position. But the real story isn't about one analyst's price target - it's about whether SK Hynix can finally escape the Korea discount and get valued like the AI infrastructure play it's become.

SK Hynix's US listing at $166 represents more than just another foreign company accessing American capital markets. It's a test of whether investors will reward the actual leaders in AI infrastructure or keep paying premiums for familiar names. HSBC's 20% upside call hinges on that valuation gap closing, and given SK Hynix's dominance in HBM memory and its position as Nvidia's key supplier, the re-rating looks overdue. The company's been building the memory that powers AI while trading at a discount - that disconnect won't survive long once US funds can easily buy the stock. Watch for the official listing date and initial trading dynamics to see if American investors are ready to pay up for the picks and shovels of the AI boom.