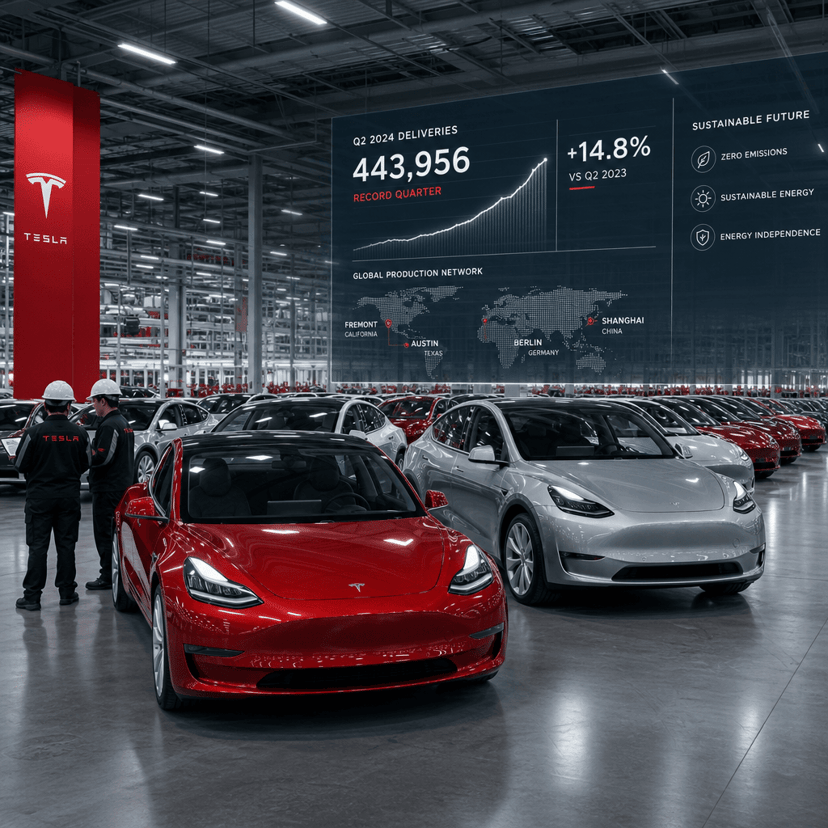

Tesla just reported 480,126 vehicle deliveries for the second quarter of 2026, topping analyst expectations and signaling potential momentum after two consecutive years of declining sales. The numbers, released Thursday, represent a critical test for CEO Elon Musk as the company attempts to rebuild consumer trust following a backlash that dragged down demand. Wall Street had been bracing for another weak quarter, making the beat all the more significant for the embattled EV giant.

Tesla is clawing its way back. The EV manufacturer just posted second-quarter deliveries of 480,126 vehicles, surpassing analyst projections and offering the first tangible evidence that its recovery strategy might actually be working. The numbers, disclosed Thursday morning according to CNBC, come at a make-or-break moment for a company that's spent the past two years watching its dominance erode.

The delivery beat matters because context is everything here. Tesla hasn't just been fighting normal competitive pressures - it's been battling a consumer revolt. The backlash against CEO Elon Musk, stemming from his increasingly polarizing public statements and social media behavior, translated directly into softening demand. Two consecutive years of annual sales declines tell that story in hard numbers. When your CEO becomes more controversial than your cars are innovative, you've got a problem that no amount of battery efficiency can solve.

But these Q2 figures suggest the bleeding might be slowing. Deliveries in the 480,000 range indicate that Tesla's core product lineup - the Model 3, Model Y, and higher-end S and X variants - still resonates with enough buyers to move serious volume. The company has been pushing aggressive incentives, expanded financing options, and strategic price adjustments throughout 2026. Those tactics appear to be gaining traction, even if they're eating into the premium margins Tesla enjoyed during its growth heyday.

The timing couldn't be more crucial. Tesla faces intensifying competition from every direction. Traditional automakers like Ford and GM have finally gotten serious about EVs, while Chinese manufacturers like BYD are flooding global markets with cheaper alternatives. Meanwhile, startup rivals that once seemed like long shots are now shipping real products. The EV market Tesla essentially created has become viciously competitive, and maintaining volume leadership requires constant execution.

Production capacity hasn't been Tesla's issue - it's been converting that capacity into actual customer orders. The company's Gigafactories in Texas, Berlin, and Shanghai can crank out vehicles at impressive rates. What's been missing is consistent demand that matches that production capability. These Q2 delivery numbers suggest the gap between what Tesla can build and what customers want to buy is narrowing, at least for now.

The Musk factor remains the wildcard nobody can quite quantify. His acquisition and subsequent management of X (formerly Twitter) alienated significant portions of Tesla's historically progressive customer base. When your brand identity centers on environmental consciousness and forward-thinking technology, having a CEO who generates daily controversy creates cognitive dissonance for potential buyers. Some analysts have argued this "Musk discount" shaved 10-15% off Tesla's addressable market. If these delivery numbers hold up, it might mean the company is successfully reaching beyond its original demographic or that the controversy is finally fading into background noise.

Wall Street will dissect these figures obsessively over the coming days. The headline delivery number is encouraging, but investors want to see the underlying health metrics. What did Tesla sacrifice in terms of pricing and incentives to hit this volume? Are margins holding steady or compressing? How much of this success came from North America versus international markets, particularly China where competition is most intense? The full earnings report, expected later this month, will provide those answers.

For now, though, Tesla has bought itself some breathing room. The company needed to demonstrate it could still execute on the fundamentals - building desirable vehicles and getting them into customer driveways - regardless of the surrounding noise. These Q2 numbers do exactly that. Whether this represents a genuine inflection point or just a temporary reprieve depends on what happens next. Tesla has to prove it can sustain this momentum through the second half of 2026 and into 2027, when several new competitors are slated to launch.

The broader EV industry will be watching just as closely as Tesla investors. As the sector's longtime leader and most visible brand, Tesla's trajectory influences everything from supplier pricing to charging infrastructure investment to consumer perception of electric vehicles generally. A sustained Tesla recovery would validate the entire category. Continued struggles would raise uncomfortable questions about whether the EV transition is happening as quickly as proponents claim.

Tesla's Q2 delivery beat offers the first concrete evidence that the company can navigate through its most turbulent period in years. But one strong quarter doesn't erase two years of declining sales or resolve the fundamental tension between Musk's increasingly controversial public persona and Tesla's need to appeal to mainstream car buyers. The real test comes in Q3 and Q4, when seasonal patterns and new competitive launches will reveal whether this is a genuine recovery or just a brief rally. For an industry watching Tesla's every move, these numbers provide cautious optimism - but the road ahead remains anything but certain.