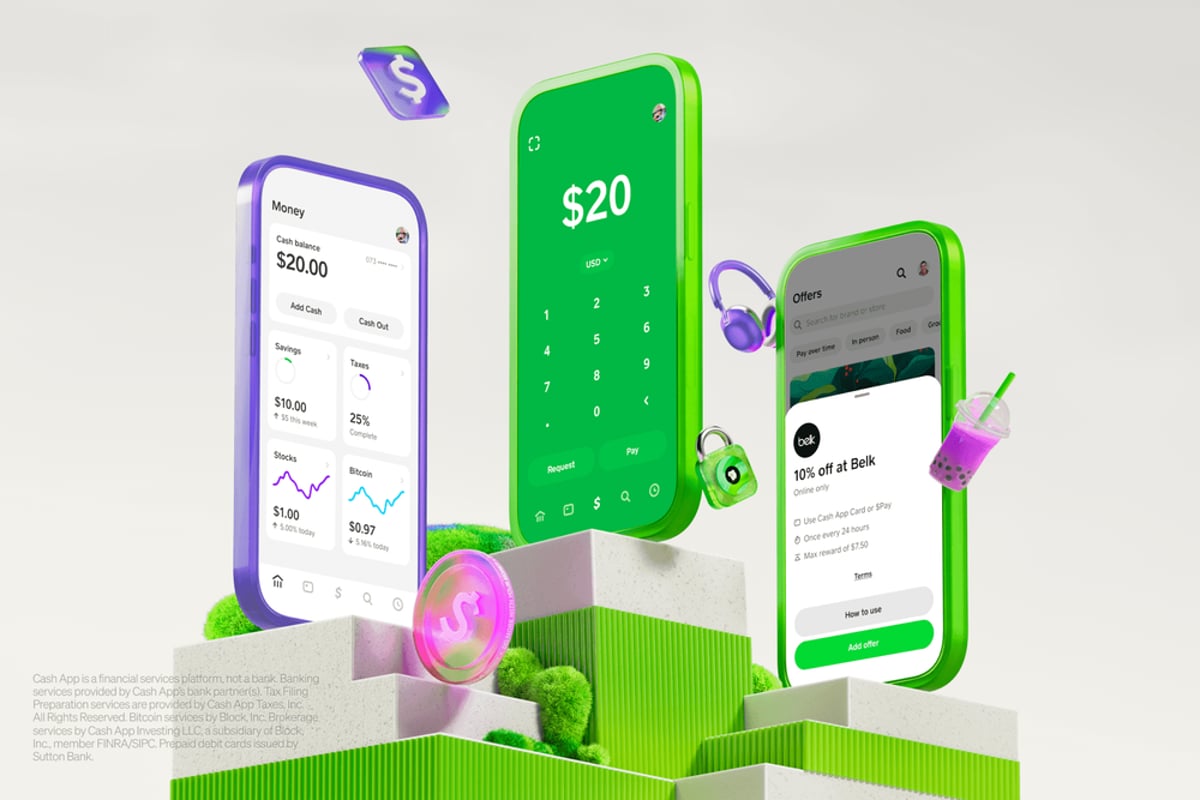

Cash App, owned by Block, is jumping into the mobile carrier business with a $40-per-month unlimited 5G plan. The move mirrors Klarna's 2025 playbook almost perfectly - same backend provider, identical pricing, even the same AT&T network infrastructure. It's rolling out to select users now, with broader availability coming in the next few months as the fintech giant tries to become the everything app for its user base.

Cash App just became the latest fintech company to bet that your phone bill belongs in your banking app. Block's payment platform announced Cash App Mobile today, an unlimited 5G wireless plan for $40 per month that includes all taxes and fees. If this sounds familiar, that's because it's essentially a copy-paste of what Klarna did last year.

The service runs as an MVNO - mobile virtual network operator - on AT&T's network and uses Gigs as its infrastructure backbone. That's the exact same setup Klarna launched with in 2025, down to the $40 price point. According to Cash App's press release, the service is "rolling out to select users, with broader availability planned in the coming months."

What makes this more than just another discount carrier clone is how Cash App plans to weave mobile service into its existing ecosystem. The company says it's building connections to Cash App Green, its rewards program, and Cash App Families, which lets parents manage supervised accounts for kids and teens. That integration layer is where things get interesting - imagine earning cash back on your phone bill or managing your teenager's data plan right next to their allowance.

Cash App positions itself as the number one personal finance app in the US, which gives it a massive built-in customer base to pitch on bundling services. The logic is straightforward: if users are already trusting Cash App with their money, why not add another monthly subscription to the mix? It's the fintech version of Amazon's playbook - start with one service, then make it sticky by adding more.

The timing follows a broader trend of non-traditional companies muscling into the wireless market. Klarna proved the model works when it launched its own MVNO last year with the help of Gigs. That company specializes in white-label mobile infrastructure, essentially letting any brand become a phone company without building the underlying network. It's the same strategy behind MVNOs like Mint Mobile or Visible, but aimed at companies that already have strong customer relationships in other verticals.

What Cash App and Klarna are really selling isn't unlimited data - it's ecosystem lock-in. The more services a user consolidates into one app, the harder it becomes to switch. Your phone bill starts appearing in the same place as your direct deposit, your peer-to-peer payments, and your debit card. That kind of integration creates friction that traditional carriers can't match.

The $40 price point positions Cash App Mobile in the middle of the prepaid market. It's cheaper than postpaid plans from major carriers but not aggressively undercutting established MVNOs. The bet seems to be that convenience and integration matter more than having the absolute lowest price. For Cash App users who already manage most of their finances through the app, switching phone carriers might just mean clicking a few buttons rather than dealing with a new company entirely.

But there are questions about how much demand actually exists for fintech-branded phone service. Klarna's MVNO launched to relatively quiet reception, and there's limited public data on how many customers have signed up. The MVNO market is already crowded with players offering similar unlimited plans, often at lower prices. Cash App's advantage is distribution - it can push notifications to millions of existing users - but that doesn't guarantee they'll bite.

The limited rollout suggests Cash App is testing the waters before committing to a full-scale launch. That's a smart move given the operational complexity of running a mobile service, even with Gigs handling the infrastructure. Customer support for wireless issues is different from handling payment disputes, and Cash App will need to staff up accordingly.

What's also notable is what Cash App isn't saying. There's no mention of exclusive features like international roaming bundles, family plan discounts, or device financing - all areas where traditional carriers and established MVNOs have built out robust offerings. The announcement focuses heavily on ecosystem integration, which suggests that's where Cash App sees its competitive edge.

The fintech-to-mobile pipeline is starting to look like a real category. First Klarna, now Cash App - it wouldn't be surprising to see other financial apps follow suit if this model proves out. The question is whether consumers actually want their bank and phone company to be the same entity, or if this is a solution looking for a problem.

Cash App's move into mobile service is less about disrupting wireless and more about building a deeper moat around its fintech business. By copying Klarna's approach with Gigs infrastructure and matching the $40 price point, Cash App is making a calculated bet that convenience beats innovation. The real test will be whether users want their phone bill and bank account living in the same app, or if this is just another feature destined to get lost in an already crowded interface. With a cautious rollout and ecosystem-first strategy, Cash App seems to understand this is an experiment - one that could either cement its position as an everything app or become a costly distraction from its core payments business.