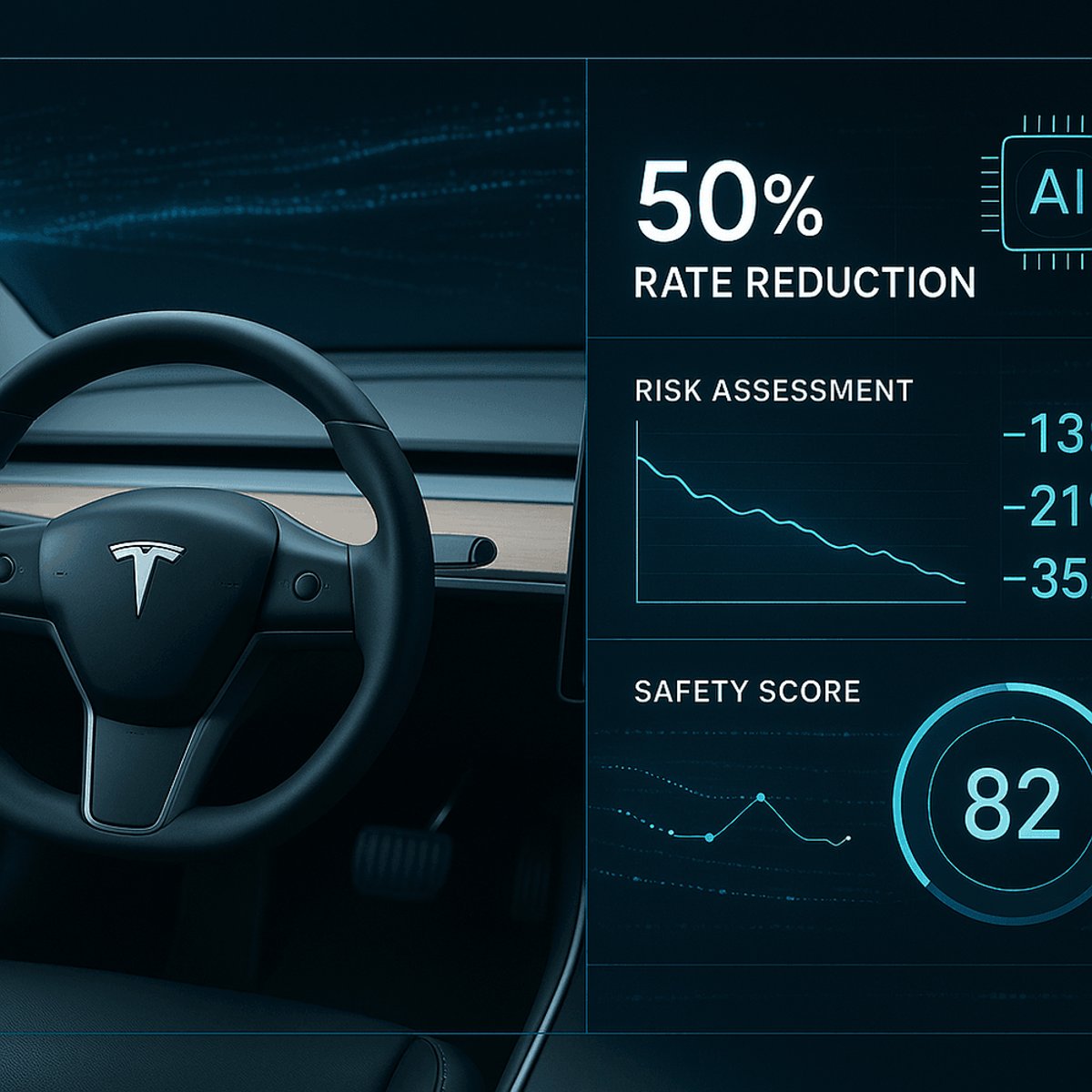

Lemonade is calling it 'Autonomous Car insurance,' and it's a bet that Tesla CEO Elon Musk actually delivers on his long-delayed promise. On Wednesday, the digital insurance startup unveiled a new product specifically for drivers using Tesla's Full Self-Driving system, promising to cut per-mile rates by approximately 50%. It's one of the first insurance products priced around how AI handles driving rather than treating autonomous features like any other car feature.

The move signals how the insurance industry is scrambling to adapt to a world where partial autonomy and true self-driving could actually become mainstream. Lemonade, which already runs a pay-per-mile insurance model that collects real driving data, is essentially building a new category here: insurance that gets cheaper the safer the AI software becomes.

The mechanics are straightforward in theory. Lemonade said it's leveraging "vehicle telemetry data that was previously unavailable" thanks to working directly with Tesla. The insurance company will train its own risk prediction models to detect when Full Self-Driving is active versus when a human driver is in control, then price accordingly. The more a Tesla's FSD software handles the driving, the lower the rates drop.

"Traditional insurers treat a Tesla like any other car, and AI like any other driver," Shai Wininger, Lemonade's co-founder and president, said in a statement. "But a driver who can see 360 degrees, never gets drowsy, and reacts in milliseconds isn't like any other driver. Our existing pay-per-mile product has given us something no traditional insurer has: a unique tech stack designed to collect massive amounts of real driving data for precise, dynamic pricing."

That framing matters because it reveals what Lemonade is really doing here - betting that FSD's safety improvements are real and measurable, and that this data advantage can be monetized. The company's existing auto insurance is already available in ten states: Arizona, California, Colorado, Illinois, Indiana, Ohio, Oregon, Tennessee, Texas, and Washington. The new FSD-specific product launches in Arizona on January 26, with Oregon following in February.

What's critical to understand is that Tesla doesn't currently offer fully autonomous vehicles. Drivers still need to be ready to take over at any moment, which is why the system is called "Full Self-Driving (Supervised)." But this product is transparently a bet on Musk's repeated promises about true autonomy eventually becoming reality. If and when that happens, Lemonade's rates would theoretically continue dropping.

There's also a competitive angle here. Tesla has been selling its own car insurance to customers for years, but the company ran into serious regulatory headwinds in late 2025. California's Department of Insurance hit the automaker with an enforcement action alleging "egregious delays in responding to policyholder claims," "unreasonable denials," and unfair claims settlement practices. Tesla has denied those allegations, but the hit raised questions about whether the company wanted to continue betting big on insurance as a business.

Enter Lemonade. By focusing specifically on FSD customers and tying insurance pricing directly to telemetry data, the InsurTech startup is essentially doing what traditional insurance companies won't: treating autonomous vehicle software as a meaningful variable in risk assessment. It's a recognition that the old actuarial models don't work when a significant portion of driving decisions are delegated to AI.

The bigger picture is about ecosystem lock-in. If Lemonade becomes the standard insurance provider for FSD users because it offers rates that actually reward safer driving patterns, it deepens customer commitment to the Tesla platform. And the data Lemonade collects through this partnership gives Tesla another window into how its vehicles are being used in the real world - information that could feed directly back into improving FSD itself.

The insurance industry's traditional approach of treating every car as essentially equivalent, regardless of its autonomous capabilities, is already looking outdated. This product launch suggests that won't hold for much longer. As autonomous features become more prevalent and more capable, insurance pricing will increasingly be determined by the software's track record rather than the car itself.

Lemonade's bet on insuring AI-driven cars reveals how the autonomous vehicle moment is forcing entire industries to rethink their playbook. This isn't just about insurance pricing - it's about who gets to own the data stream from increasingly autonomous vehicles, and whether software performance can actually become a sellable feature. For Tesla, it's validation that FSD matters enough for third parties to build entire products around it. For the insurance industry, it's a warning that the actuarial models of the past won't survive the shift toward autonomous driving.