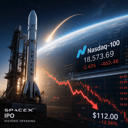

The euphoria has faded. One month after SpaceX made history with the largest tech IPO in a decade, investors are getting their first hard look at how Elon Musk's rocket company actually makes money - and the picture is more complicated than the launch-day hype suggested. According to BBC News, the reality of SpaceX's revenue streams has come into sharper focus, revealing a business still heavily dependent on government contracts even as it pitches itself as the future of commercial spaceflight.

SpaceX went public in June 2026 with all the fanfare befitting a company that's landed rockets on floating platforms and ferried astronauts to the International Space Station. The IPO raised $8.5 billion at a valuation north of $150 billion, making it the biggest tech debut since Meta went public. Institutional investors couldn't get enough exposure to what they saw as the next chapter in commercial space exploration.

But now, four weeks into life as a public company, the champagne has gone flat. According to BBC News analysis, mandatory financial disclosures are painting a more nuanced picture of how SpaceX generates revenue - and it's not quite the purely commercial space operation that retail investors might have imagined. The company's quarterly filings reveal that government contracts, particularly from NASA and the Department of Defense, still account for a substantial portion of incoming cash, even as the Starlink satellite internet business grows.

This isn't necessarily a red flag - Boeing and Lockheed Martin have built decades-long businesses on government aerospace contracts. But SpaceX positioned itself differently during the IPO roadshow, emphasizing its commercial launch dominance and the revolutionary potential of Starlink to bring internet to underserved markets worldwide. The disconnect between that narrative and the actual revenue breakdown has some early investors reconsidering their positions.

The timing is tricky. SpaceX went public just as the broader market started questioning sky-high valuations for growth-stage tech companies. Amazon competitor Rivian saw its stock plummet 70% in the year following its IPO when production challenges emerged. Tesla itself went through years of volatility before reaching sustainable profitability. Now SpaceX faces similar scrutiny, with analysts demanding clear paths to profitability beyond the excitement of rocket landings.

Starlink represents the commercial wild card. The satellite internet constellation has over 5,000 satellites in orbit and claims more than 2.3 million subscribers globally. But the unit economics remain murky - launching and maintaining that constellation costs billions, and subscriber growth in developed markets has been slower than projected. Rural and maritime customers love the service, but urban adoption hasn't materialized as quickly as the pre-IPO investor deck suggested.

Meanwhile, Blue Origin, backed by Amazon founder Jeff Bezos, is ramping up its own commercial ambitions with the New Glenn rocket. Rocket Lab continues chipping away at the small satellite launch market. And traditional aerospace giants are finally taking reusable rockets seriously after years of dismissing the technology. The competitive landscape SpaceX faces as a public company is far more crowded than when it first disrupted the industry a decade ago.

Wall Street's patience for growth stories has shortened dramatically. Public market investors want to see consistent revenue growth, improving margins, and realistic timelines for ambitious projects like the Starship Mars missions. The quarterly earnings treadmill is unforgiving, especially for a company that's spent years operating with the flexibility of private ownership. Elon Musk famously resisted taking SpaceX public for years, precisely because he didn't want quarterly pressures interfering with long-term Mars colonization goals.

The coming months will test whether SpaceX can balance those competing demands. The company has a strong record of execution - it's the only private entity launching astronauts and has fundamentally changed launch economics through reusability. But transforming that operational excellence into predictable public company performance is a different challenge entirely. Early investors who bought on IPO day hype are now confronting the reality that even revolutionary companies need sustainable business models.

What happens next depends largely on Starlink's trajectory and whether SpaceX can convert its technological advantages into commercial launch contracts that offset government revenue dependence. The company has ambitious plans to dramatically increase Starship launch cadence, which could lower costs further and open new markets. But those are still plans, not realized revenue - and public markets trade on results, not potential.

The SpaceX IPO story is entering its awkward second act - the part where initial excitement meets quarterly earnings reality. Investors who bought into the Mars colonization dream are now parsing government contract percentages and Starlink subscriber acquisition costs. That's not inherently bad - it's just the difference between being a visionary private company and a public one that needs to explain itself every 90 days. Whether SpaceX can satisfy both Wall Street's demands and Musk's interplanetary ambitions will define the next chapter of this story. For now, the honeymoon is clearly over.